Don't Fight the Fed

February 15, 2022

“Don’t Fight the Fed” – an old Wall Street reminder not to get in the path of the Federal Reserve. With the Fed shifting its focus to fighting inflation, how do we stay on its good side?

The Federal Reserve’s most notable function is controlling the overnight lending rate – known as the Fed Funds Rate. By maneuvering this rate up or down, the Fed works to maintain maximum employment and stable prices. Walking the tight rope between these two is the Fed’s balancing act.

With the economy now back on solid footing after the Covid recovery, the Fed is shifting course, moving from a very accommodative stance (low rates) to a tightening campaign (higher rates). Covid caused a never-before-seen shock to the national employment picture, with 22.1 million jobs lost between January and April of 20201. Thanks to nearly two years of unprecedented monetary stimulus, the economy has recovered, and unemployment is back down to 4.0%, which is about as good as it gets.

The same monetary stimulus that helped during the dark days of Covid is now pushing prices up, causing the highest inflation in 40 years. Consumer prices (CPI) are growing at a +7.5% annual rate, well above the Fed’s comfort zone. While there remains some debate on how much of the recent jump in prices is “transitory,” the Fed is no longer comfortable watching prices run higher.

To fight rampant inflation, the Fed plans to start raising short-term interest rates, possibly as soon as March. The market is pricing in five rate hikes this year, taking the overnight rate up from 0% to 1.25% or higher. This is designed to pump the breaks on the economy. Higher rates will slow money velocity (number of times a dollar gets used in the economy), which will slow the pace of price increases. This is exactly what Fed Chairman Paul Volcker did in the early 1980s to combat double-digit inflation.

Unlike the early 1980s, when the Fed pledged to break inflation even if it pushed us into recession (which it did), the current Fed wants to engineer a goldilocks scenario. They raise rates just enough so that employment stays healthy, inflation moderates, and the economy keeps growing – everything is “just right.”

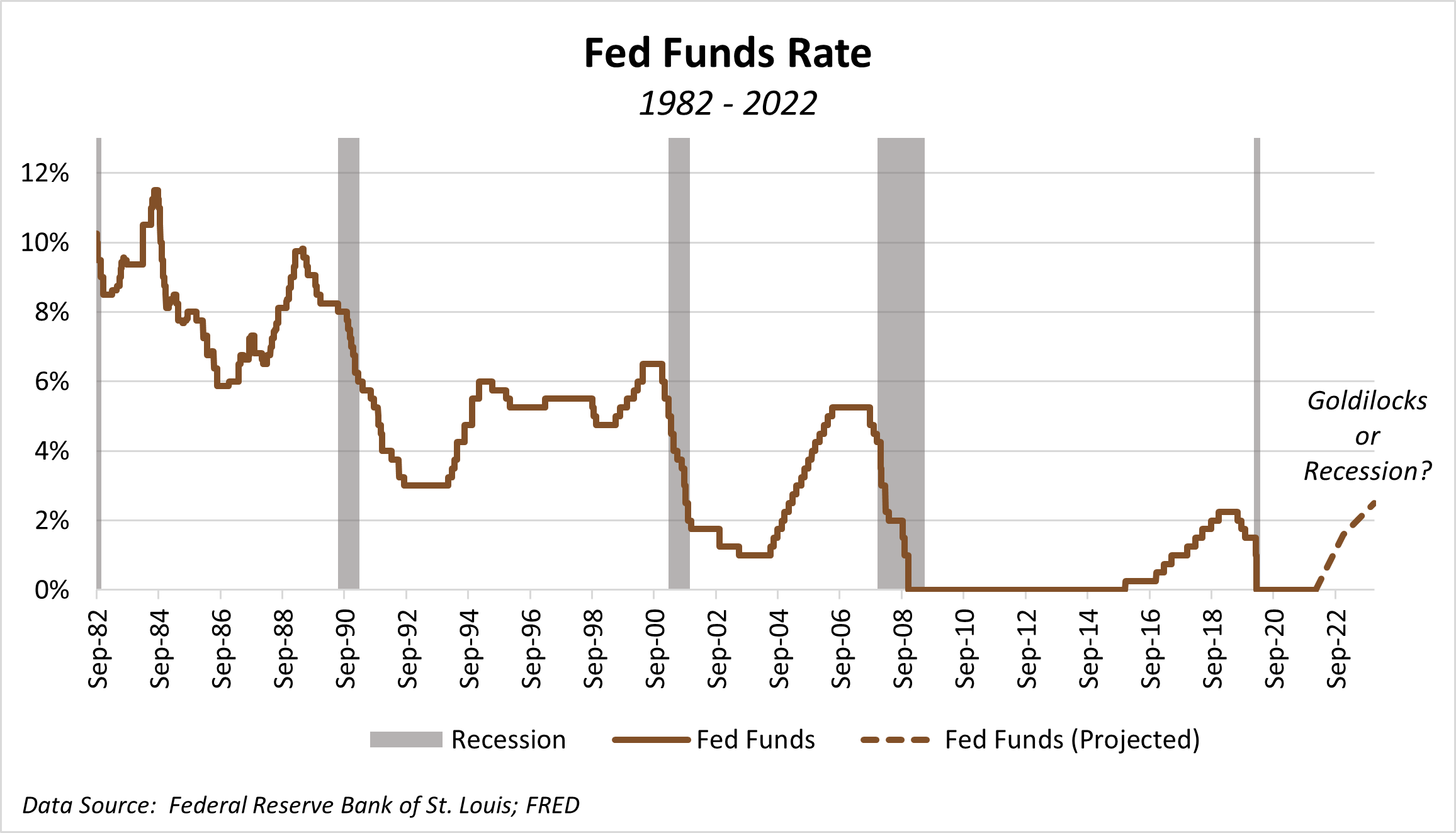

The market is skeptical given the historic correlation between Fed tightening and the start of a recession. As the graph above shows, Fed rate tightening campaigns usually occur shortly before an economic downturn. Some economists attribute 11 of the last 12 economic recessions to Fed tightening2. While a tightening campaign is needed to combat inflation, there may be ugly consequences.

Interest rates are already moving up in anticipation of the Fed. The 2-year Treasury bond is approaching 1.6%, its highest level since pre-Covid. Long-rates, like the 10-Year Treasury are also rising, nearing 2%, the highest level since 2019. We continue to position accounts in high-quality, short-dated bonds; ones with the low-price risk and near-term maturities to allow us to participate in rising rates.

While higher rates directly impact bonds, there are ripple effects on the stock market. Rising mortgage rates, which are up 0.75% this year already, can slow the red-hot housing market, which is boosting large swaths of the economy. Higher rates also impact how companies finance themselves, affecting everyone from Main Street to the Fortune 500.

One area where higher rates have a big influence is on company valuations. Not to get in the weeds of corporate valuation, but as rates rise the value of future cash flows is worth less today (due to a higher discount rate). This impacts growth stocks the most. Companies not earning anything today, but with expectations to be profitable years down the road see large valuation shifts due to rate changes.

This is what happened in January – as concern grew that the Fed would tighten, analysts factored in higher rates and found growth stocks to be worth less. This caused the tech heavy Nasdaq Index to sell off -16.8% from its November peak to the late January low. The Dow Jones Industrial Average, which is focused on blue-chip companies that are profitable today, wasn’t impacted as much by rising rate expectations, and was only off -7.1% from peak to late January.

As the Fed begins its first-rate tightening campaign since 2016, we view the best portfolio positioning to be in high-quality stocks and short-term bonds. Whether the Fed succeeds in engineering a goldilocks scenario or pushes us into a recession, value stocks are attractively priced. They come with historic stability and the defensiveness to potentially outperform in good times, inflation environments, or downturns. An overweight to value positions also keeps us from “fighting the Fed.”

If you have any questions about your account(s), or if there has been a change in your financial situation or investment objectives, please feel free to contact any member of our team at (406) 839-2037 to schedule a meeting.

1 Congressional Research Service report “Unemployment Rates During the Covid-19 Pandemic,” 8/20/21; https://sgp.fas.org/crs/misc/R46554.pdf

2 Barron’s article “Forget About Inflation. Contrarians Expect a Recession and a Drop in Bond Yields,” 2/7/22; https://www.barrons.com/articles/inflation-recession-bond-yields-51643997182?refsec=up-and-down-wall-street

Data Sources: St. Louis Federal Reserve FRED Database; Koyfin